U.S. economic data is generally outperforming expectations, resulting in solid economic growth supported by a resilient consumer, massive capital spending on artificial intelligence (AI) infrastructure, productivity gains, lower tax rates and tax law changes promoting business investment.

A stronger labor market has been an encouraging development, with the last three monthly employment reports showing job growth averaging nearly 190,000 per month, after accounting for revisions. Additionally, the weekly initial jobless claims data, which only counts individuals who file for unemployment for the first time that week, have been near their lowest levels since the late 1960s.

Our base case is U.S. economic growth will remain solid, but the ability of AI leaders to monetize their investments and increase earnings enough to justify their rich valuations remains uncertain. In the long run, we think AI will not just provide ongoing productivity gains but will ultimately prove revolutionary. Nevertheless, expectations are high, and bouts of uncertainty will lead to volatility, such as the sharp decline in the S&P 500® Index in early June.

Inflation remains an ongoing concern. It has been above the U.S. Federal Reserve’s (Fed) 2% target since 2021, raising concerns that inflation expectations could rise, risking a self-fulfilling prophecy. Despite excluding the more volatile food and energy prices, the Core Consumer Price Index (CPI) and Core Personal Consumption Expenditures (PCE) Price Index have risen steadily since February. While oil prices have fallen recently, we expect continued uncertainty about the conflict in the Middle East, solid consumer spending and strong demand for AI infrastructure, such as semiconductors and computing equipment, to keep core inflation above the Fed’s 2% target.

After the Fed’s June meeting, new Chairman Kevin Warsh was notably more hawkish (focusing more on inflation risks than stimulating economic growth) than the market was expecting, with nine of the committee’s 18 members projecting at least one interest-rate hike by the end of the year, including six members who projected more than one hike. We believe the Fed is likely to raise rates this year, possibly as soon as the September meeting, given the recent rise in core inflation and our expectation that Chairman Warsh will want to signal his commitment to combating inflation.

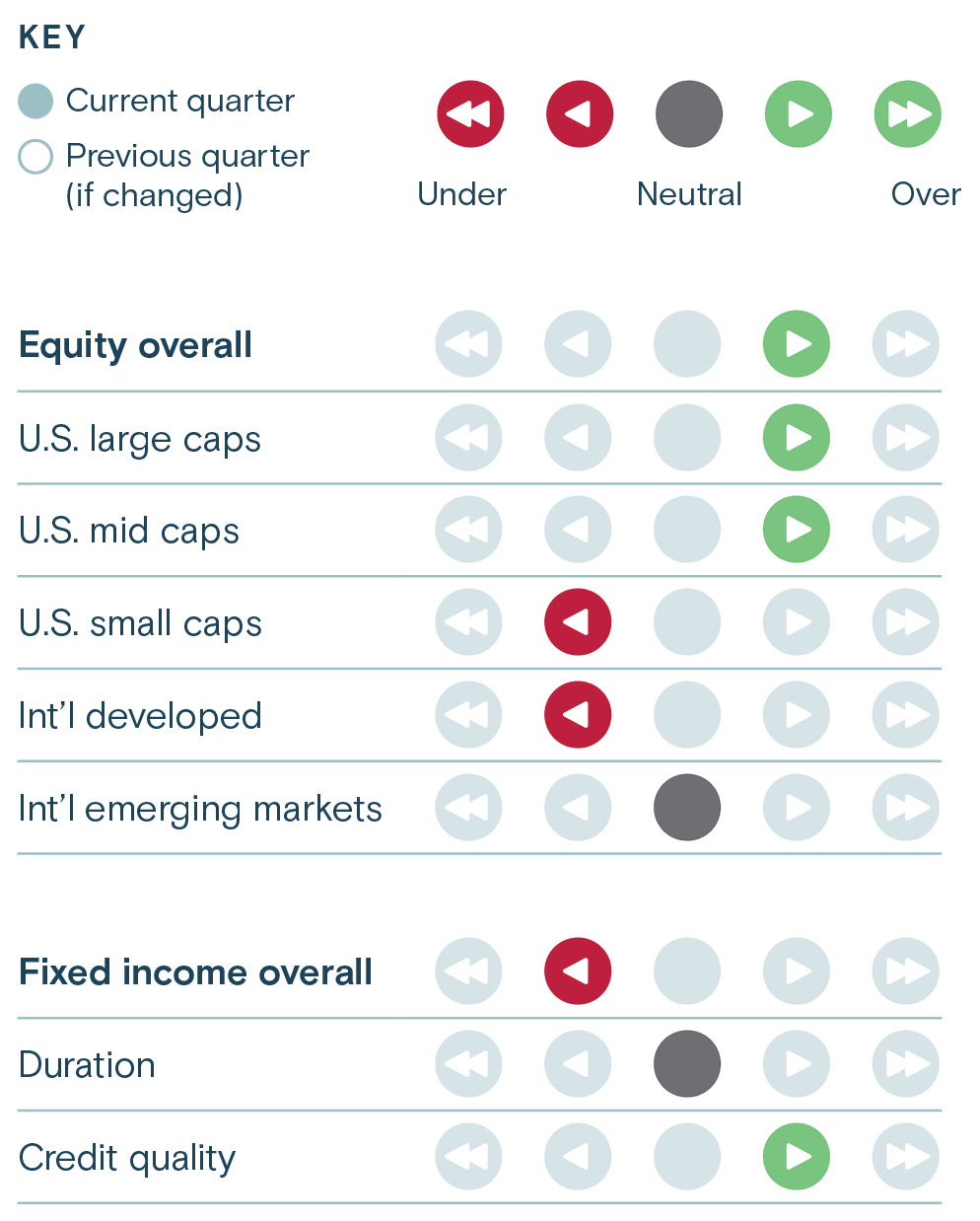

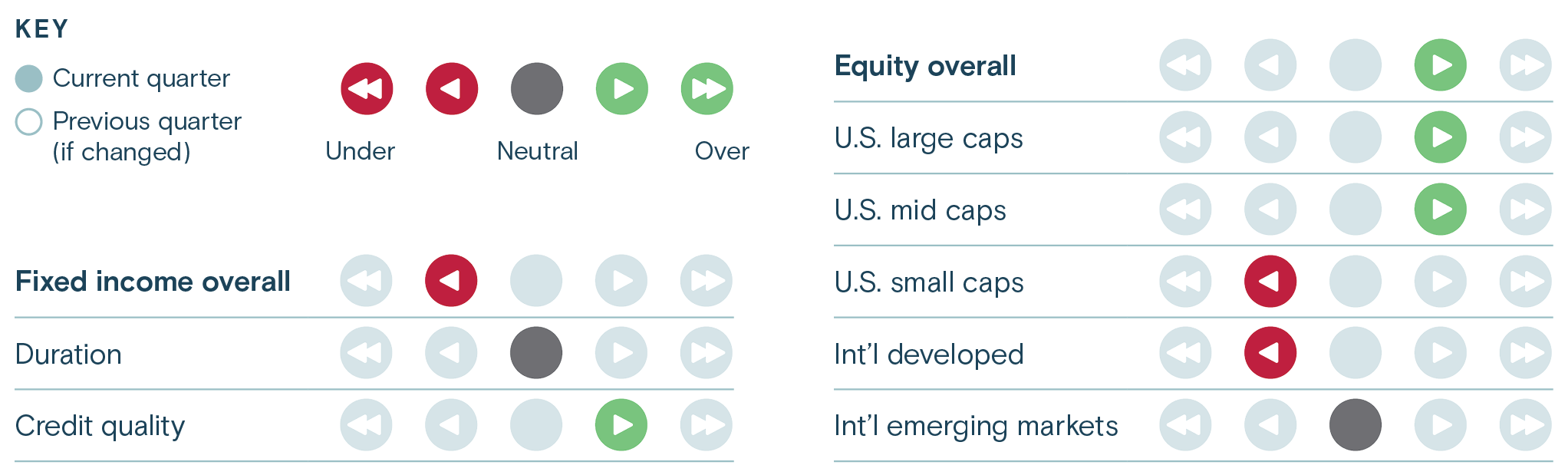

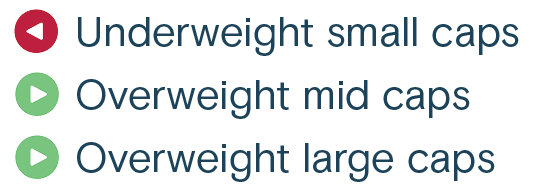

Given our broadly constructive outlook, we continue to recommend maintaining exposure to U.S. equities, favoring an overweight to large-cap stocks and a moderate overweight to mid-cap stocks as we expect continued strength to broaden. In fixed income, we expect modest flattening of the yield curve, favoring longer-dated Treasury securities and higher-quality corporate bonds. Investment-grade corporate bond spreads (the yield paid over comparable Treasuries) are relatively narrow, but as their absolute yields remain attractive, we expect continued demand.

![Small caps: Earnings improvements meet attractive valuations [VIDEO]](/content/dam/thrivent/fp/fp-insights/fund-commentary/small-caps-earnings-improvements-meet-attractive-valuations/small-caps-earnings-improvements-meet-attractive-valuations-thumb.png/_jcr_content/renditions/cq5dam.web.1280.1280.jpeg)

![2026 Mid-Year Market Outlook [PODCAST]](/content/dam/thrivent/fp/fp-insights/advisors-market360-podcast/advisors-market360-podcast-16x9-branding-insights-card.jpg/_jcr_content/renditions/cq5dam.web.1280.1280.jpeg)